The Australian dollar has proven stubbornly resilient in recent months, thanks to firm iron ore prices and reluctance on the part of the United States Federal Reserve to raise US interest rates. This note updates our valuation model of the Australian dollar, particularly in light of recent comments by the Reserve Bank suggesting the terms of trade may have already bottomed. Based on the analysis, my year-end call for the A$ is 0.72c, declining to 0.68c by mid-2017.

On traditional valuation grounds, the $A is now only modestly overvalued

After briefly touching my target of US68c in January this year, the Australian dollar has been remarkably resilient in 2016, generally trading north of US75c. Several factors have been at play: fears of US interest rate hikes have generally eased, and thanks to Chinese policy support (and probably speculative excess), spot iron ore prices have also held up surprisingly well. Going the other way, however, has been the fact the Reserve Bank has cut official interest rates from 2% to 1.5%.

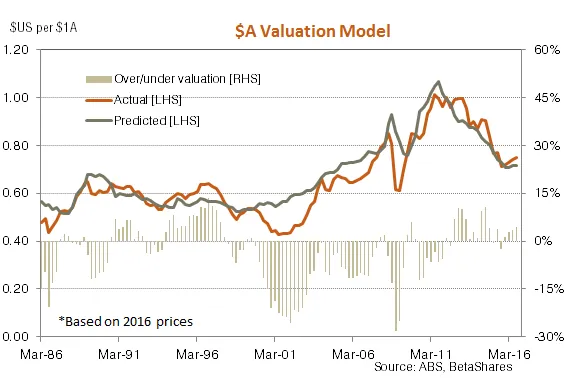

All this begs the question: where are we now with regard to the $A’s “fundamental” valuation? We have previously considered this question using a valuation model similar that most favoured by the RBA, which is based on the terms of trade (price of exports relative to imports) and real (i.e. after inflation) short-term interest rate differentials between Australia and international peers.

Using the latest available data, such a valuation model suggests fair-value for the $A versus the $US would be currently US72c – which implies a 4% over valuation given the $A is currently around US75c.

By the standard of recent years, the $A is still overvalued, but not to the degree seen in late 2012/early 2013 and again in mid-2014 – when overvaluation was around 10%.

Will the negative forces on the $A wane?

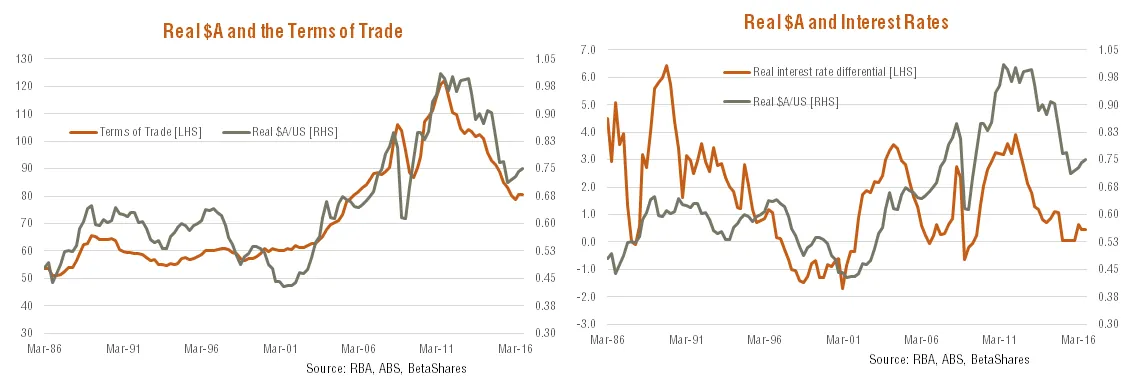

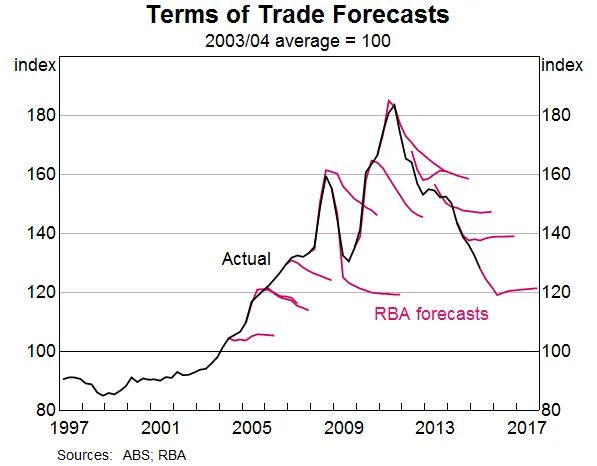

What’s more, the RBA’s latest forecasts now project the terms of trade will remain “close to current levels” over its 2-year forecasting horizon. If so, it means the terms of trade should no longer have a significant negative near-term influence on the $A going forward, leaving only an anticipated narrowing in the spread between US and Australian interest rates – due particularly to higher US interest rates – as the major lingering negative influence. That said, the model suggest interest rates effects are quite modest compared to terms of trade effects. Indeed, as seen in the chart below, while there has been a reasonable strong positive relationship between the terms of trade and the real exchange rate over time – the influence of interest rates has been somewhat looser.

In fact, the model suggests that a 1% rise in US short term interest rates – which in itself would be a very aggressive move within a year – would, all else constant, only lower fair-value for the $A to around US70c. All up, if the RBA is right and the traditional valuation model holds, the $A may struggle to break through US70c anytime soon.

Broader valuation suggests the $A should fall further

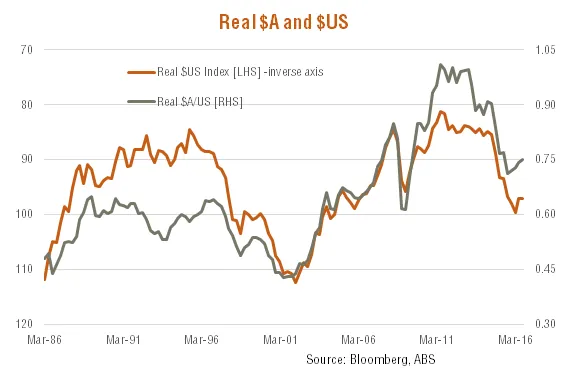

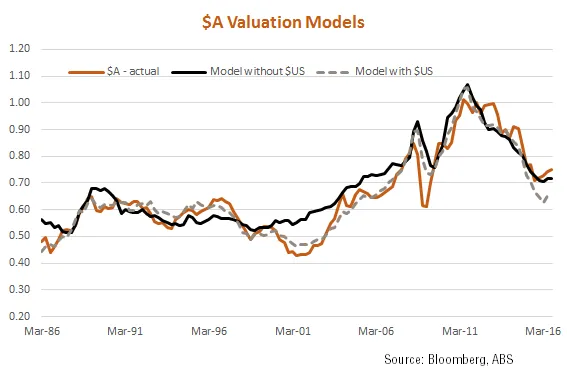

Another remarkable feature of $A trends over time, however, is that there has also been a close negative relationship with trends in the US dollar. Indeed, including the real $US exchange rate index into the valuation model above significantly improves the model’s fit, with the $US having a significant negative influence. Much of the $A movement over time therefore appears to reflect broader trends in the world’s leading currency, the $US. This is clearly evident in the chart below.

Indeed, as seen in the chart below, with the real $US included in the above model, historical relationships suggest fair-value for the $A is now closer to US65c – due to the current relative strength in the US dollar. If the $US holds at current levels and/or lifts further – possibly due to higher US interest rates – this extended valuation model suggests the $A should fall further.

It should also be noted that the RBA’s track record with regard to forecasting the terms of trade has not been great – though arguably not much worse than many other forecasters. The RBA underestimated the terms of trade rise during the commodity boom and, so far at least, has tended to underestimate the decline in the terms of trade during the commodity downturn. That suggests we should take the RBA’s latest terms of trade forecast with a grain of salt.

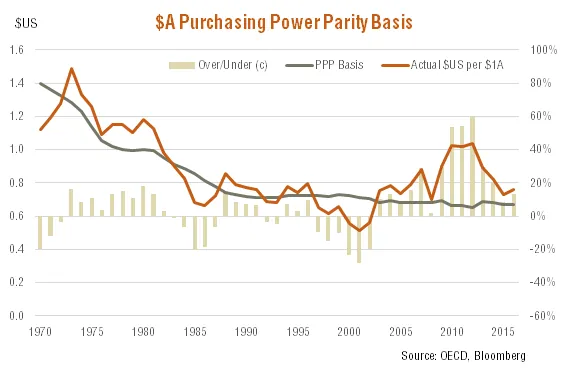

Last but not least, it’s also worth remembering that on a purchasing power parity (PPP) basis (i.e. allowing for the higher general cost of producing output in Australia versus that of the United States), fair-value for the $A remains closer to US68c. The $A has tended to broadly track its PPP value over time, though with cycles of over and under valuation. The recent period of significant PPP over valuation – due to the commodity price boom – could easily give way to a period of PPP under valuation.

All up, the resilience of the $A so far this year is consistent with the surprising firmness in commodity prices and the reluctance of the Fed to raise interest rates. That said, based on the view that commodity prices and the terms of trade will likely fall further, and that US interest rates and the US dollar will likely rise, there still seems more downside that upside risk to the $A from current levels. A sub-US70c $A value would also be consistent with long-run purchasing power parity.

In view of recent $A resilience, however, my year-end call is revised somewhat higher to US72c (from US68c), with a decline to around US68c now expected by mid-2017.

This post was originally published at the BetaShares Blog at www.betasharesblog.com.au/aud-still-overvalued

David Bassanese is the Chief Economist for BetaShares. BetaShares is an Australian manager of funds which are traded on the Australian Securities Exchange. BetaShares offers a range of exchange traded funds which cover Australian and international equities, cash, currencies, commodities and alternative strategies. Author website: www.betashares.com.au/insights/author/david-bassanese

QuietGrowth has been publishing content in this blog or in other sections of the website. Contributors for this content may include the employees of QuietGrowth, or third-party firms, or third-party authors. Unless otherwise noted, such content does not necessarily represent the actual views or opinions of QuietGrowth or any of its employees, directors, or officers.

Any links provided in our website to other websites are for the purpose of convenience, or as required by any such other websites. Unless otherwise noted, this does not imply that QuietGrowth endorses, is affiliated, and/or promotes any information, or products or services of those websites. Please read the advice disclaimer section of the website too.