Dividend Income has been Relatively Attractive and Stable

The good news for Australian investors is that the local share market still offers attractive income returns, provided they are prepared to stomach the volatility in share price performance. And despite recent downward pressure on corporate earnings, most companies seem likely to preserve their dividend returns to the maximum extent possible.

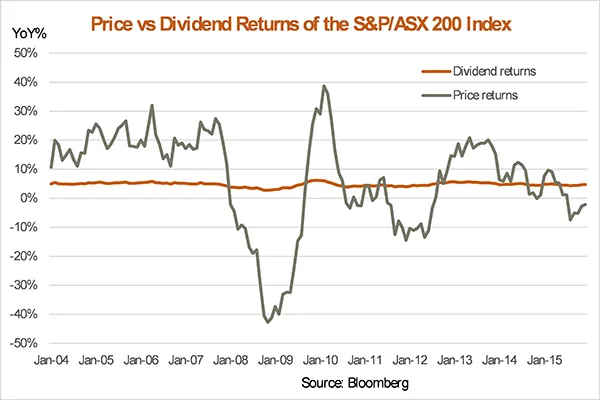

Dividends have been the quiet achiever of the Australian equity market, contributing significantly to the total return of the market over time. In the 12 years to the end of 2015 the compound annualised return for the S&P/ASX 200 was 8.8 per cent, while the price index produced 3.2 per cent – implying dividends produced 5.6 per cent per annum – or two-thirds of the market’s total return over the period.

Dividend returns have also been considerably less volatile. The standard deviation in rolling 12-month price returns for the S&P/ASX 200 Index over the same period above was 17 per cent per annum. The worst 12-month price performance was a 42.7 per cent decline in the year to the end of November 2008; the best performance was a 38.7 per cent gain in the year to the end of February 2010.

By contrast, the standard deviation in rolling 12-month dividend returns (the difference in annual performance of the market’s total return and price indices) over this period was only 0.7 per cent per annum. The worst annual dividend return (before dividend imputation) was 2.7 per cent in the year to the end of 2008; the best performance was 6.2 per cent in the year to the end of December 2009.

Even in the darkest of times, investors can expect at least some dividend return. Dividends keep on keeping on.

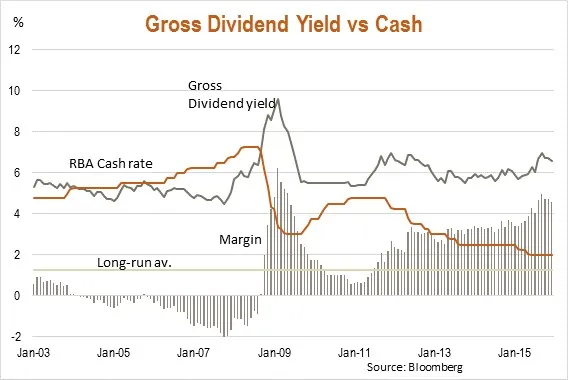

Over 2015 the dividend return from the market (as measured by the S&P/ASX 200 Index) was 4.7 per cent. The grossed-up dividend return (after accounting for franking credits) was 6.5 per cent, more than three times the Reserve Bank’s official cash rate of 2 per cent.

The chart below shows that relative to interest rates, the market’s current grossed-up dividend yield remains attractive.

Indeed, the only time the yield looked more attractive was when market valuations sank to very cheap levels at the bottom of the 2008-09 Global Financial Crisis. At the end of December 2015, the gross dividend yield was 6.6 per cent per annum, compared to only around 2.5 per cent for the MSCI World (Developed Market) Equity Index (excluding Australia).

Of course, all this begs the question whether dividend payments are sustainable against the backdrop of weak local economic growth and subdued corporate earnings. Recent market speculation, for example, has suggested that both BHP Billiton and ANZ Bank – for their own unique reasons – may need to cut their dividends, given asset writedowns.

For investors concerned with the overall market, however, it remains the case that many companies place great importance on maintaining dividend payments to the extent possible, even if this means a rise in payout ratios at a time of cyclically depressed earnings.

According to Bloomberg estimates, the average payout ratio (the proportion of earnings paid out as dividends) for companies in the S&P/ASX 200 Index has edged up to 90 per cent in recent years, compared to a longer-run average of around 75 per cent. Unless earnings recover, that suggests the level of dividends may not be sustainable and will need to be cut.

But provided there remains a reasonable prospect of an earnings recovery, many companies seem well placed to maintain dividends at least for the foreseeable future.

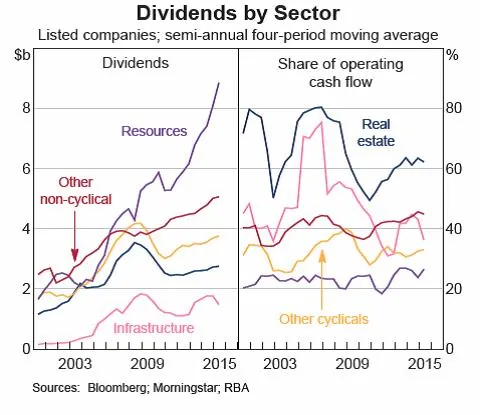

Indeed, according to recent research by the Reserve Bank of Australia (Trends in Australian Corporate Financing, RBA Bulletin December 2015), “[listed] companies have generally increased dividends over recent years, after the reduction in dividend payments immediately following the global financial crisis.” The RBA notes that while companies have increased dividends as a share of operating cash flows in recent years, this ratio remains “well within historical norms”.

All up, assuming dividends do not need to be slashed, the market’s prospective income returns should remain attractive for yield-hungry investors this year, especially as interest rates should not rise by much. Although the US Federal Reserve is likely to modestly raise official interest rates this year, overall global inflation remains low, which should contain the overall rise in bond yields.

Closer to home, moreover, the bias for official interest rates remains to the downside, given weakness in mining investment and commodity prices, together with emerging signs that the home-building boom has peaked.

David Bassanese is the Chief Economist for BetaShares. BetaShares is an Australian manager of funds which are traded on the Australian Securities Exchange. BetaShares offers a range of exchange traded funds which cover Australian and international equities, cash, currencies, commodities and alternative strategies. Author website: www.betashares.com.au/insights/author/david-bassanese

This post was originally published at the BetaShares Blog at www.betasharesblog.com.au/dividends-the-quiet-achiever