Contrary to the hopes of both the Reserve Bank of Australia and the Federal Treasury, economic growth is off to a bad start in 2017 so far. Importantly, however, the recent Federal Budget included new powers for the Australian Prudential Regulation Authority to impose geographic-based lending restrictions. If used, these new restrictions could allow scope for the Reserve Bank to further support the economy through lower interest rates later this year if need be, with less risk of further inflaming the already hot Sydney property market.

2017: So far so bad

In its latest Quarterly Statement on Monetary Policy, the Reserve Bank of Australia continued to present a relatively upbeat outlook for the economy. In particular, the RBA expects the economy to grow by around 3% over the course of 2017 and that the unemployment rate will tend to decline. By contrast, I have presented a case where the economy retains at least three downside risks with regard to dwelling construction, mining investment and consumer spending.

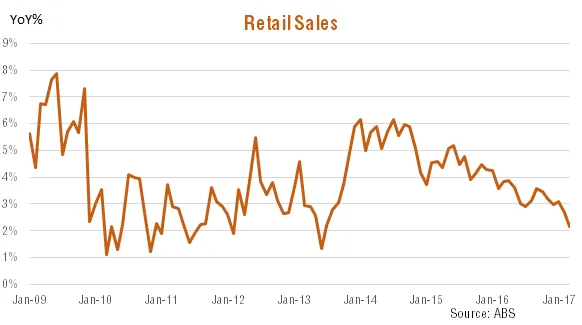

In recent weeks, some of these risks have begun to play out. For starters, consumer confidence has taken a tumble with households finally reacting to persistent weakness in income growth and growing fears about a correction in property prices. Associated with this concern, annual growth in retail spending to end-March has slowed to 2.1% – its weakest pace in four years.

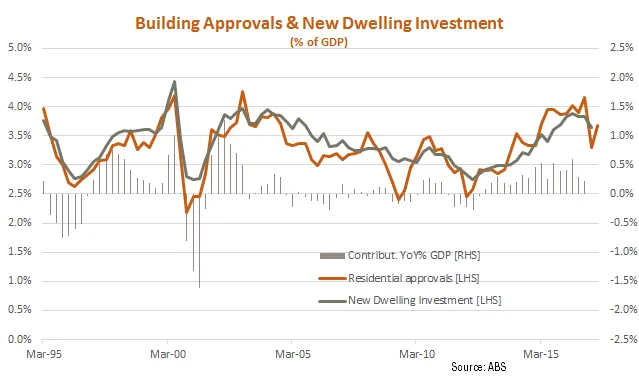

Meanwhile, contrary to RBA hopes that a backlog of high-rise apartment developments would hold up housing activity for some time – despite the clear decline in approvals over the past year – private residential construction activity surprised on the downside in the March quarter, falling 4.6%. As seen in the chart below, even allowing for a possible backlog of work, the trend in building activity is already clearly downward, suggesting further declines seem likely if building approvals also continue to fall.

All up, there is a very real risk of close to flat GDP growth in the March quarter, and potentially even a negative result. Meanwhile, Cyclone Debbie seems likely to detract at least 0.25% from June quarter growth due to reduced agricultural output, coal exports and tourism. While such weather related events can be considered a “one-off” it comes at an unfortunately vulnerable time given the already tepid pace of underlying momentum in the economy.

Geographic Restrictions?

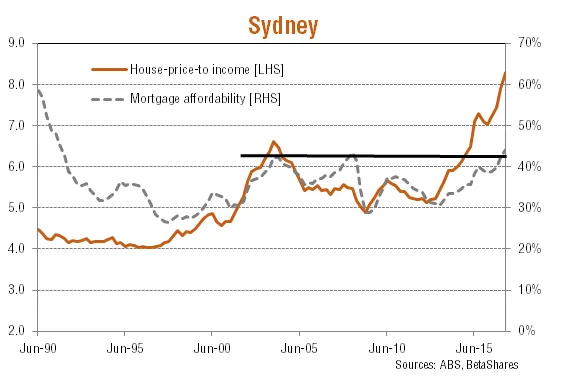

Despite this weakness, the RBA remains a “reluctant rate cutter” due to concerns that this would add to upward pressure on property prices in the already hot markets of Sydney and Melbourne. As seen in the chart below, my home affordability measures* suggest Sydney property prices relative to household income were by the end of the March quarter already well above previous cyclical highs. Allowing for today’s relatively low mortgage rates, moreover, mortgage costs associated with buying a median-price Sydney home are also now back at previous cyclical highs. This suggests mortgage affordability costs – together with recent credit tightening measures by private banks – could soon start to slow Sydney house price gains.

That said, if Sydney house prices continue to rise inexorably, it’s worth noting that as part of this month’s Federal Budget, Treasurer Scott Morrison announced new powers by which APRA could specially direct banks (and non-banks) to limit lending in certain geographic areas. If exercised, this could help deal with the problem whereby current across the board “macro-prudential” lending restrictions don’t allow for the quite divergent housing conditions across the country. Such geographically based measures could also help reduce current RBA concerns that another rate cut – while potentially beneficial for the wider economy – might unduly add to pressure in some already hot property markets.

Investment implications

These developments are worth watching closely. If the economy continues to generally disappoint while continued strength in the Sydney (and/or Melbourne) property markets cause APRA to launch a new round of geographically based lending restrictions, the case for another RBA rate cut as early as Melbourne Cup day could fall into place. In the least, recent weakness in the economy – and APRA’s new capacity to directly tackle the Sydney property market – suggests its very unlikely the RBA would contemplate a rate hike anytime soon.

Notwithstanding potentially higher long-term bond yields – due to better global growth – this suggests the search for yield in the local equity market is likely to remain intense. Given the risk that “bond proxy” sectors of the market – like listed property and infrastructure – could be hurt by rising bond yields, yield-conscious investors might prefer financial sector exposure (such as through QFN) or specific income enhancement strategies (such as through HVST or YMAX).

This post was originally published at the BetaShares Blog at www.betashares.com.au/insights/lending-restrictions-provide-scope-lower-interest-rates

David Bassanese is the Chief Economist for BetaShares. BetaShares is an Australian manager of funds which are traded on the Australian Securities Exchange. BetaShares offers a range of exchange traded funds which cover Australian and international equities, cash, currencies, commodities and alternative strategies. Author website: www.betashares.com.au/insights/author/david-bassanese

QuietGrowth has been publishing content in this blog or in other sections of the website. Contributors for this content may include the employees of QuietGrowth, or third-party firms, or third-party authors. Unless otherwise noted, such content does not necessarily represent the actual views or opinions of QuietGrowth or any of its employees, directors, or officers.

Any links provided in our website to other websites are for the purpose of convenience, or as required by any such other websites. Unless otherwise noted, this does not imply that QuietGrowth endorses, is affiliated, and/or promotes any information, or products or services of those websites. Please read the advice disclaimer section of the website too.